April 28, 2026

The invoice answers one question about AI. The operating budget answers the rest.

Cloud taught the industry an important lesson: variable technology spend needs a management discipline, not just a procurement process. FinOps became the language for that, helping institutions match purchasing to real usage, monitor consumption as it changes, and correct quickly when cost and value stop moving together.

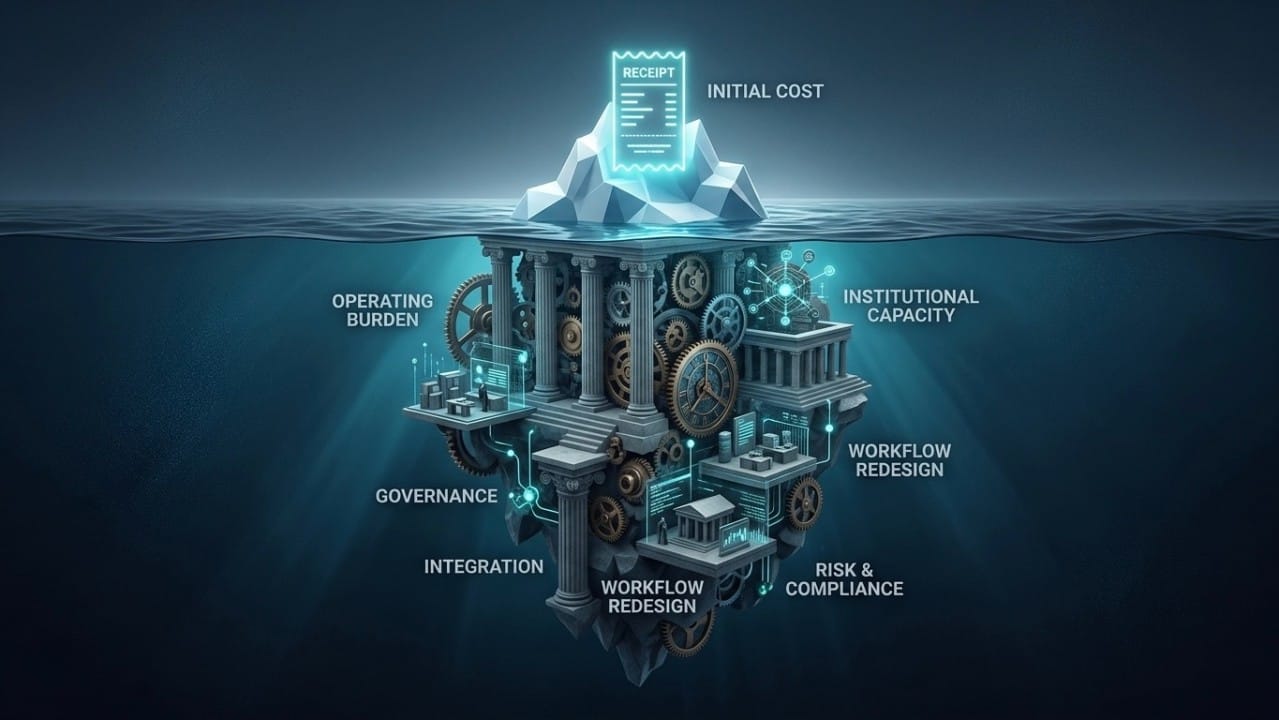

That is why so many AI business cases feel complete at approval and incomplete six months later. The launch cost is usually visible enough: licensing, implementation, configuration, maybe a pilot. What is less visible is what it takes to run the capability well once it is live.

Some of that is straightforward operating cost. Some AI expenses are relatively fixed. Others rise with use. The more activity runs through the tool, the more workflows it touches, the more outputs it generates, the more the run cost can move. That means a successful use case can become more expensive precisely because it is succeeding.

Boards do not need a lesson in token pricing to govern that well. They need a clearer financial question: which costs stay stable, which costs scale with usage, and what happens to the budget if adoption doubles faster than expected? That is a much better conversation than treating AI like a flat software subscription.

Then there is the work that does not arrive as a clean invoice.

AI creates operating burden. Integration. Monitoring. Exception handling. Workflow redesign. Staff training. Policy interpretation. Ongoing refinement. Someone has to review outputs, answer questions, step in when the tool behaves unexpectedly, and make sure the process still works for members and staff.

Some of that shows up as direct spend. A lot of it shows up as institutional capacity. Time from operations leaders. Attention from risk and compliance. Support from data and technology teams. Effort from managers and frontline staff. In other words, part of the cost of AI is not just what you buy. It is what the organization has to carry.

That is where a lot of institutions get surprised. The software budget is approved. The operating model is assumed. And assumptions are usually cheaper on paper than they are in practice.

This is also where sourcing can create false comfort. Vendor-delivered AI can make the capability feel lighter because the model sits inside a broader product relationship. However, the institution still owns the outcomes. The oversight, the governance, the member impact, and the exception handling do not stay with the vendor just because the technology does.

For credit unions, that last part matters more than it might in other sectors. Under-resourced AI does not just create internal inefficiency. It can lead to weaker explanations, slower exception handling, more false positives, and more friction in member moments where trust matters most.

What I find more useful than a generic ROI conversation is a more grounded set of questions. What is the fully loaded cost in year one, year two, and year three? Which costs are fixed and which rise with use? What work is being assigned to existing teams, and what work is actually being funded? Where is the contingency for the integration and governance work that almost always turns out to be larger than first expected?

That is not a pessimistic frame. It is a more mature one. A business case that surfaces full cost, variable cost, and operating burden alongside projected value is not just a better finance document. It is a better governance document.

The institutions that manage AI well will not be the ones with the cheapest pilot. They will be the ones that understand what they are actually operating, what it asks of their teams, and what it will take to sustain it responsibly over time.

When your institution evaluates AI investment, which part is still least visible: the variable run cost, the governance burden, or the internal capacity required to make the tool work well?