February 18, 2026

Yesterday we explored why AI governance still matters even if your credit union is mostly buying AI through vendors instead of building models in-house. Today, let’s stay with that idea and look at a simple way to make the work feel more manageable, because most AI governance conversations assume one model, one vendor, and one clean line of ownership. In real credit union journeys, AI decisions often move through several platforms before they ever show up as an approval, denial, or cross-sell offer to a member.

Why this feels overwhelming

When AI is described as something you “build and govern,” it can sound like it only applies to institutions training their own models. Yet many credit unions are already using AI inside digital account opening, loan origination, identity verification, fraud, and cross‑sell tools, often without labeling it that way. That’s where governance starts to feel unmanageable, because it’s easy to assume each vendor “has it covered” in their part of the flow.

A more honest way to look at it is: you don’t own 100 percent of AI risk, but you own more than you might think, especially where decisions affect members and regulators. The work is figuring out what sits in your column versus your partners’ columns, and making that explicit instead of implied.

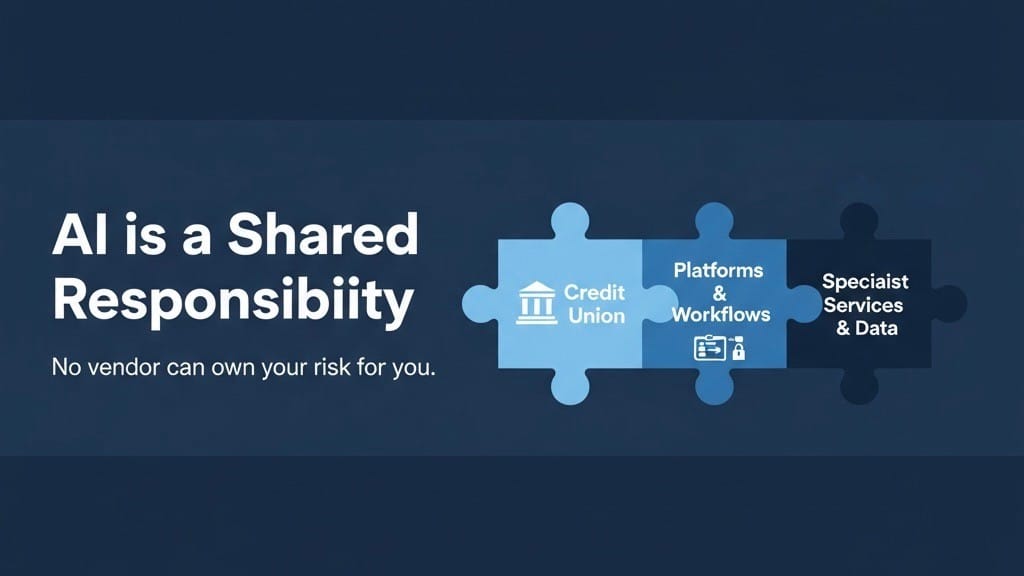

A three‑layer model as a starting point

As a practical starting point, many AI‑enabled member journeys map cleanly into three swim lanes, even if the product names and integrations differ. This isn’t a formal standard or the only way to structure responsibility, but it gives a clear frame for documenting your actual stack.

Journey owner: the institution

This is where accountability ultimately lands. This is the layer we sit closest to. We own the overall experience and outcome: who we target, what we offer, which journeys we automate, and where a human must step back in. That includes:

- Defining eligibility and risk appetite for products and cross‑sell, not letting a black box quietly redefine them.

- Deciding which partners are in the flow, what data they receive, and what they’re allowed to do with it.

- Maintaining an inventory of where AI and automated decisioning touch members, especially in credit and identity.

Orchestration and decision engines

These platforms run the logic: which offer shows up, when to call identity checks, when to push to manual review, when to present an instant decision. Their responsibilities include:

- Keeping the integrations stable so decisions aren’t silently degraded when a downstream service changes.

- Exposing configuration in a way that allows my team to tune thresholds, rules, and eligibility criteria in business language.

- Providing logs and explanations so we can reconstruct “what happened” for a given member and refine the journey.

Specialist services and data providers

Identity, fraud, and credit‑worthiness platforms do the heavy lifting of verifying who someone is and how risky a transaction might be. They’re responsible for:

- The quality and security of the checks they perform and the data sources they rely on.

- Documenting the limits of their models and signals so we don’t treat them as infallible.

In some environments, a single platform spans more than one swim lane; in others, there might be a fourth or fifth layer (for example, a separate data enrichment service). The value of this three‑layer view is not perfection; it’s that it forces us to see the journey as a set of connected responsibilities instead of a monolithic “AI system.”

What “shared responsibility” really means in this context

Once you see the layers, the shared responsibility model becomes more concrete and less abstract.

Data

- Partners are responsible for protecting the data they receive and for how they use it in their models.

- You are responsible for data quality, appropriateness, and making conscious choices about what member data you share where.

Models and logic

- Partners are responsible for how their models and rules are built, tested, and documented.

- You are responsible for deciding whether a given model or rule set is fit for your members, products, and risk appetite, and how it is configured in your environment.

Security and access

- Partners secure their platforms and APIs.

- You define who in your organization can access which tools, change which thresholds, or override which decisions.

Governance, compliance, and outcomes

- Partners may provide attestations, certifications, and generic compliance documentation.

- You remain accountable for fair lending, BSA/AML, UDAAP, and exam expectations tied to the decisions made with those tools.

In other words, partners own recommendations and infrastructure; you own how those recommendations get turned into real‑world member outcomes in your credit union.

Where organizations tend to course‑correct

Across organizations, certain patterns repeat when the stack gets more complex.

- The flow is treated as “one system,” but no one can clearly explain which platform did what at each step of a member decision.

- Risk and compliance teams get involved late, once the journey is already live, and have to reverse‑engineer who is responsible for which control.

- Contracts and oversight focus on individual vendors, while gaps live in the seams between platforms.

These are the moments that tend to trigger a pause: teams step back, map the journey end‑to‑end, clarify who sits in each swim lane, and document responsibilities in plain language rather than relying on assumptions. That work is rarely glamorous, but it’s what turns “shared responsibility” from a slide into something examiners, boards, and internal teams can actually work with.

A practical way to get started

You don’t need a massive program to begin making this real.

- Pick one AI‑enabled journey: for example, digital account opening with cross‑sell and automated decisioning.

- Draw three columns: journey owner, orchestration/decisioning, specialist services.

- For each major step, ask three questions:

- Who is acting here, and what exactly are they doing?

- Who can change the logic, thresholds, or data used at this step?

- Who is ultimately accountable if something goes wrong for a member or in an exam?

That simple exercise can surface hidden dependencies, unclear ownership, and opportunities to put better guardrails in place without slowing down innovation.

When you look at your own AI‑enabled journeys through this lens, where do you see the biggest opportunity: in mapping the end‑to‑end flow, in clarifying responsibilities across the three swim lanes, or in giving your teams clearer levers to intervene when automation and member outcomes start to drift apart?