March 4, 2026

In yesterday’s post, I talked about using journey mapping and enterprise architecture together to understand where member experiences and systems do, and do not, line up. Once that picture is clearer, the next question usually becomes: how do we decide where to invest?

Technology budget conversations can be a real opportunity when everyone is working from the same picture of what the dollars are meant to do.

In the same room, “technology spend” can legitimately mean different things: keeping members’ money and data safe, supporting growth as the organization expands, or unlocking new capabilities that make life easier for members and staff. All of those are valid. Naming them clearly tends to make the conversation more productive.

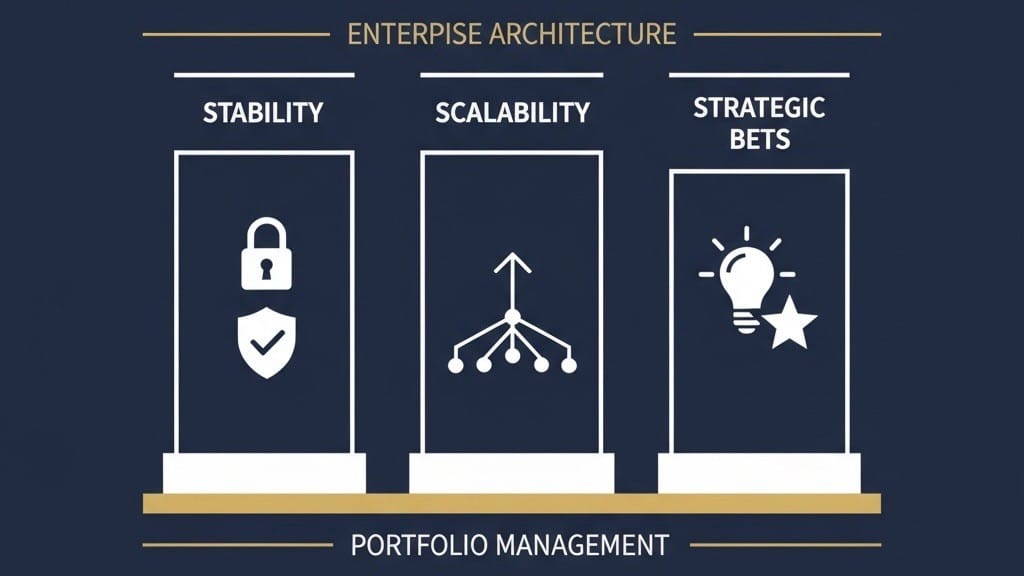

One simple way to do that is to use three buckets as shared language:

- Stability: secure, reliable, compliant operations.

- Scalability: the ability to grow members, products, and data without adding friction.

- Strategic bets: visible improvements in member or employee experience, such as faster decisions, better digital journeys, or smarter routing in the contact center.

Looking at the portfolio through this lens often highlights strengths. Many credit unions have built a very solid foundation on the stability side. Others have already taken important steps on scalability, especially around APIs and cloud adoption. And some have begun making focused strategic bets that line up nicely with their mission and strategic plan.

Enterprise architecture and technology portfolio management help turn that snapshot into ongoing progress. Enterprise architecture, which showed up yesterday from the systems side, gives a clear view of which platforms exist, how they connect, and where there are opportunities to simplify, standardize, or modernize. It can highlight places where a thoughtful integration or consolidation would free up capacity for new initiatives, or where addressing technical debt today creates room for future innovation.

Technology portfolio management adds rhythm and structure. It looks at the collection of systems and services as a portfolio that should stay aligned with business objectives, risk appetite, and member outcomes over time. That is where questions like “Is this still giving us the value we expected?” or “Is there a better way to meet this need now that our environment has evolved?” fit naturally.

The opex versus capex discussion is another place where a shared lens helps. On‑premise approaches tended to lean more on capital expenditure up front, while cloud and SaaS models show up more as operating expense over time. Neither is inherently better; they simply offer different tradeoffs:

- Cloud and SaaS can make it easier to scale, adopt new capabilities faster, and adjust as needs change.

- On‑premise can provide a clearer sense of long‑term ownership and may align well with certain risk or regulatory preferences.

When teams talk about a new investment in the context of stability, scalability, and strategic bets, and also consider how it shifts the opex/capex balance over several years, the decision often becomes clearer. The conversation moves from “Is this expensive?” to “Does this help us deliver on our strategy and serve members better, in a way that is sustainable for our size and stage?”

Every credit union will end up with a slightly different mix, and that is a good thing. The point is not to look like anyone else’s portfolio. The point is to make sure your technology investments, whether on‑premise or in the cloud, are working together in support of your mission.

If your leadership team used this lens in your next planning cycle, where would you see the most opportunity: reinforcing stability, adding scalability, or making a few focused strategic bets that members would clearly feel?