The business value belongs to finance, and the controller or CFO should define it before the capability is enabled. The outcome is tighter cost control and stronger audit readiness: catching duplicate invoices, out-of-pattern payments, and irregular journal entries early, while cutting the manual review burden that consumes the finance team. The owner is the controller or head of internal audit; the metrics are review hours saved, errors and recoveries caught before they post, and audit findings avoided. Naming the outcome matters because the value of anomaly detection is easy to feel and hard to quantify unless you decide up front what you are measuring.

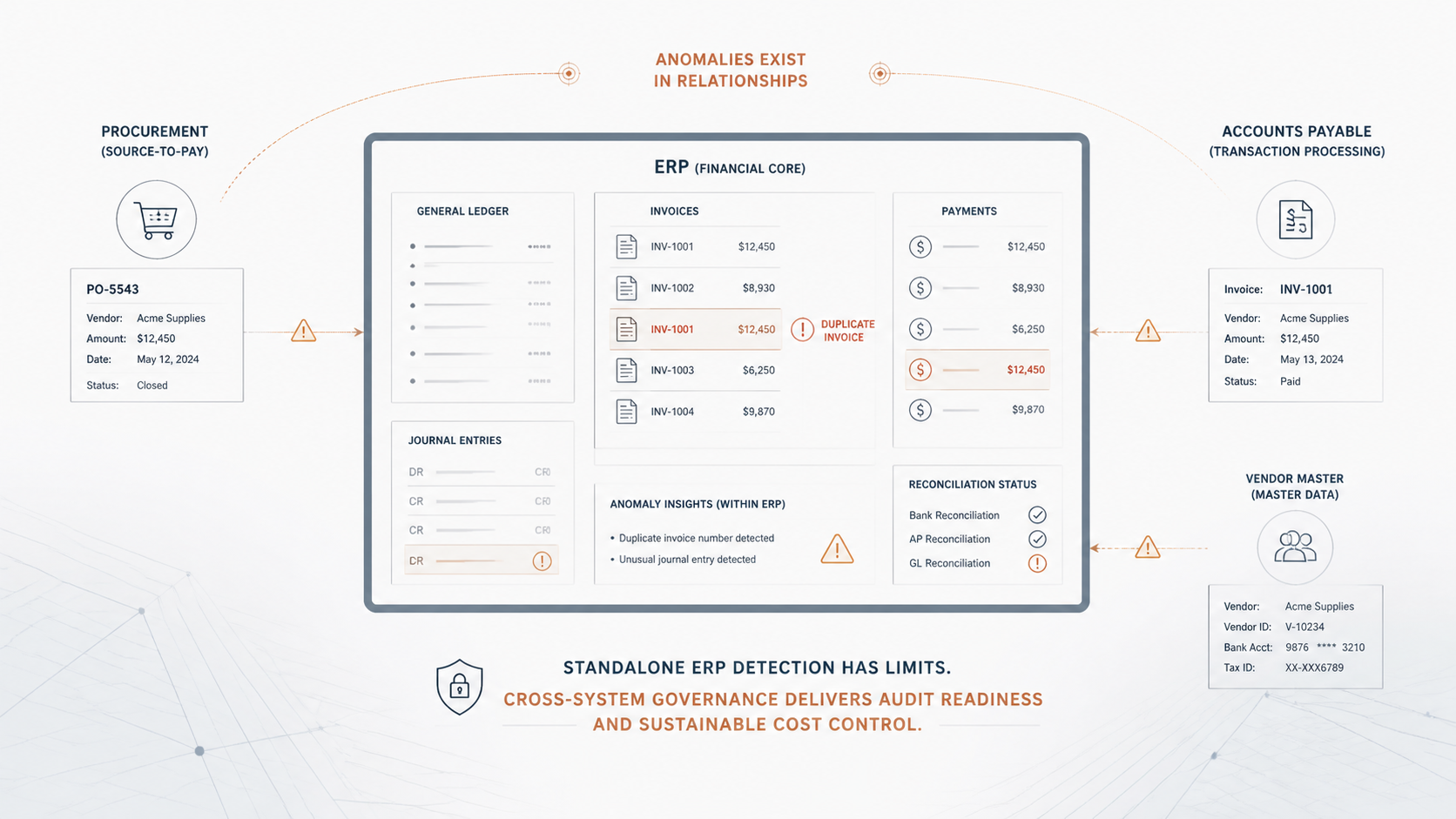

This is one of the more attainable use cases, and a good example of embedded AI working well, because it operates inside an unusually clean boundary. Modern ERPs embed anomaly detection trained on the structured, consistent financial data the system already holds and governs: AP records, general ledger entries, vendor payments, expense transactions. It sits at the easy end of the delivery range, and within the ERP boundary it is genuinely effective. The honest part of the discussion is about what that boundary excludes.

What it actually takes to deliver

Inside the ERP, delivery is mostly a matter of enabling the feature on data that is already in good shape, which is why this is a strong quick win. The model catches the anomalies that are visible in a single system: a duplicate invoice, a payment outside normal ranges, a journal entry that breaks the historical pattern of an account.

The limitation is that the most damaging financial irregularities frequently do not stay within one system. Consider a company with a procurement system, AP in the ERP, and a vendor master maintained by a separate team. A scheme worth catching might combine a quiet alteration to a vendor record, purchase orders that each look reasonable, fabricated or skipped goods receipts, and invoices that are entirely normal on their own. Inside the ERP, the AP data shows nothing alarming, because the anomaly is not in any one system. It is in the relationship between the vendor master change, the procurement pattern, and the AP flow, and no single system holds all three. The ERP-native model cannot see it, because it cannot correlate across systems it was never given. It catches the clumsy fraud and misses the sophisticated one constructed to look normal in each system it touches.

Closing that gap is a different and larger effort. It requires correlated data from procurement, AP, and the vendor master, which means resolving the vendor, the supplier, and the payee to the same real-world entity across systems with different owners and data models, governing that master data, and building lineage so an investigator can trace a flagged pattern back through all three systems. That is no longer an embedded feature; it is a cross-system data effort.

There is also a tuning reality that decides whether either version gets used at all. Anomaly detection produces false positives, and the rate is not incidental; it determines whether the finance team trusts the alerts or learns to dismiss them. Set the threshold too tight and real irregularities slip through. Set it too loose and the team drowns in flags that turn out to be ordinary, and within a few weeks they treat every alert as noise. Getting this right means tuning against your own transaction patterns and giving someone ownership of the alert queue and the review thresholds, so sensitivity is adjusted deliberately rather than left at a default that fits no one. The embedded version still needs this; it simply needs it on one system's data rather than three.

What to ask, prepare, and implement

Ask whether your coverage needs to extend to irregularities that look normal within each system but anomalous across systems, because that determines whether the embedded feature is sufficient or only a starting point. Prepare by confirming the ERP data the model uses is sound, which it usually is, and by being clear-eyed that the clean win inside the ERP does not cover the boundary-crossing risk. If cross-system detection is needed, implement entity resolution and governed master data for vendors and suppliers first, since correlation is impossible without it, and design lineage so any cross-system alert can be traced to source records for investigation.

Resources to make it land

On people and roles, the embedded version needs a finance process owner and the internal audit team to act on alerts; it does not require a data science build. The cross-system version adds a data engineer for integration, a master data owner accountable for vendor and supplier identity, and an investigative analyst who can work a correlated alert. On skills and external help, the ERP-native capability is a configuration and process exercise within reach of finance systems staff. The cross-system extension calls for master data management and data integration skills, where outside help is often warranted, particularly for entity resolution across procurement, AP, and vendor systems. On data work and tooling, the embedded version leans on the ERP's own feature and existing data quality. The cross-system version requires integrating procurement, AP, and vendor master data, resolving entities to common identifiers, governing that master data, and lineage to support investigation.

The readiness questions are these. Does your fraud and error exposure include schemes that look normal within each individual system but anomalous across systems? Are your vendor and supplier entities resolved to common identifiers with governed master data? If the embedded feature covers your real risk, deploy it now and take the value. If your exposure crosses system boundaries, the question is whether you are prepared to do the master data and integration work before an incident proves the gap was where the real risk lived.