February 17, 2026

Most AI governance advice assumes you’re building models in-house.

If I’m hearing most discussions correctly, in general credit unions are just trying to understand the AI already hidden in their vendors’ roadmaps.

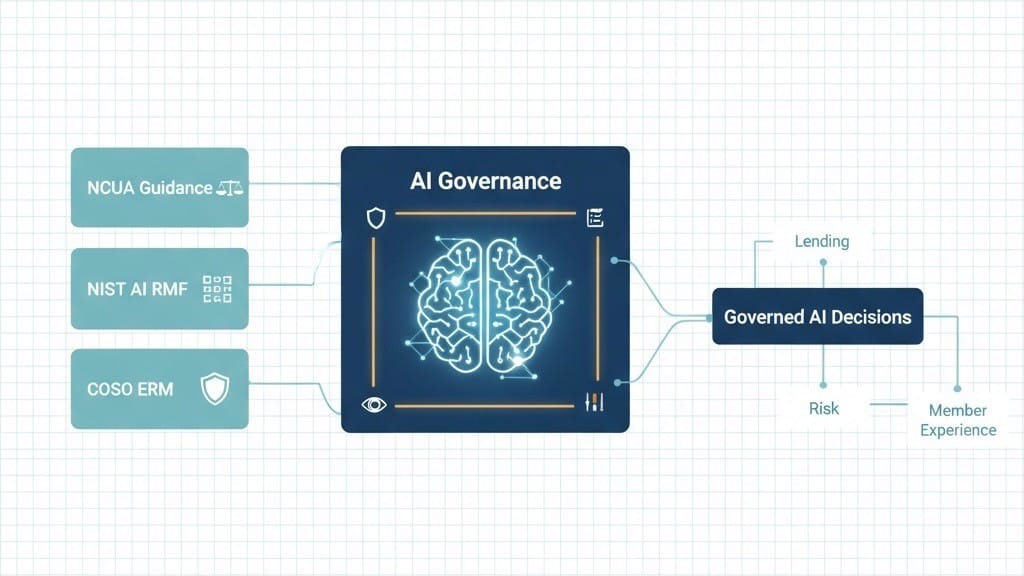

That gap creates a weird tension. On one side, regulators and frameworks are getting clearer that AI governance matters whether you build or buy. On the other, a lot of day-to-day AI in our world shows up as a release note from a core, LOS, or digital banking provider. It’s easy to treat that like a feature toggle, not a risk and governance question.

If AI touches members, it’s our governance problem

If AI is changing a member outcome, it’s our governance problem, even if the model lives in a vendor’s data center.

- A loan denial doesn’t feel “vendor-owned” to the member who gets the message.

- A card block at the grocery store doesn’t feel “third-party model risk” to the family at checkout.

- A chatbot giving a shaky answer doesn’t feel like “NLP drift” to a member in financial stress.

The model might be theirs. The relationship, trust, and accountability are still ours. It is our reputation at risk.

“We bought it” isn’t a governance strategy

A lot of AI risk guidance points back to the same basic idea: inventory, classify, apply extra discipline where the impact is high. You don’t need a separate AI bureaucracy to start doing that with vendor AI.

- Make a list of every place AI is influencing decisions or communication credit, fraud, chat, collections, ID verification, marketing.

- For each one, write down in plain language what could go wrong for a member if it misfires, and what that would mean for exams and reputation.

- Decide which of those belong in the “high impact” bucket where you want stronger controls: more human review, clearer override policies, tighter monitoring.

None of that requires building models or standing up an “AI center.” It does require admitting that “the vendor said it’s fine” isn’t enough anymore.

I’d be willing to bet that many skim right past the “AI-powered” language in vendor decks. If uptime and integration looked good, did you mentally put it in the “tech plumbing” category? Understandable, but consider asking a different set of questions:

- Where does this AI actually change an outcome for a member or employee?

- If it goes wrong at scale, what story would I need to tell my board and examiner?

- Do we have a real way to pause, override, or adjust it if we’re uncomfortable?

That mindset shift is probably more important than any specific framework. Once you see AI as part of your everyday risk and member experience decisions, governance stops being an “extra” and starts looking like normal leadership.

So I’m curious: when you look at the AI already embedded in your vendors, what’s one place where your current level of oversight doesn’t match the potential impact on members and risk and what would a modest, realistic step-up in governance look like in your context, not an idealized one?